"This imaginary person out there - Mr. Market - he's

kind of a drunken psycho. Some days he gets very enthused, some days he gets

very depressed. And when he gets really enthused, you sell to him and if he

gets depressed you buy from him. There's no moral taint attached to that."

- Warren

Buffett

“The big money is not in the buying and selling. But in the

waiting.” - Charlie Munger, Vice Chairman, Berkshire Hathaway

EXISTING HOME SALES

Americans stepped up their home

purchases in June by a robust 20.7% after the pandemic had

caused sales to crater in the prior three months. But the housing market could

struggle to rebound further in the face of the resurgent viral outbreak and a

shrinking supply of homes for sale.” Story at…

My cmt: A 3% 30-yr mortgage doesn’t hurt either.

EIA CRUDE INVENTORIES (Energy Information Administration)

“U.S. commercial crude oil inventories (excluding those

in the Strategic Petroleum Reserve) increased by 4.9 million barrels from the

previous week. At 536.6 million barrels, U.S. crude oil inventories are about

19% above the five year average for this time of year.” Press release at…

My cmt: …which explains the drop in the energy sector

today.

ATA TRUCK TONNAGE (ATA)

“American Trucking Associations’ advanced seasonally

adjusted (SA) For-Hire Truck Tonnage Index increased 8.7% in June after falling

1% in May. In June, the index equaled 115.3 (2015=100) compared with 106.1 in

May.

“Not surprisingly, as more states lifted restrictions in June, truck tonnage was robust,” said ATA Chief Economist Bob Costello. “While the gain in June was the single best month since January 2013, the solid gain was not enough to put tonnage back to pre-pandemic levels, but it is close. I am hearing good anecdotal freight reports for July, but I am concerned that freight could slow as more states reinstate restrictions due to increasing Coronavirus cases.”

15 BULLISH FACTORS…OR NOT (Real Investment Advice)

“…#12. Valuations don’t matter. Just the Fed….

{kind=link}

…#15. This time is different...”

Charts and Commentary at…

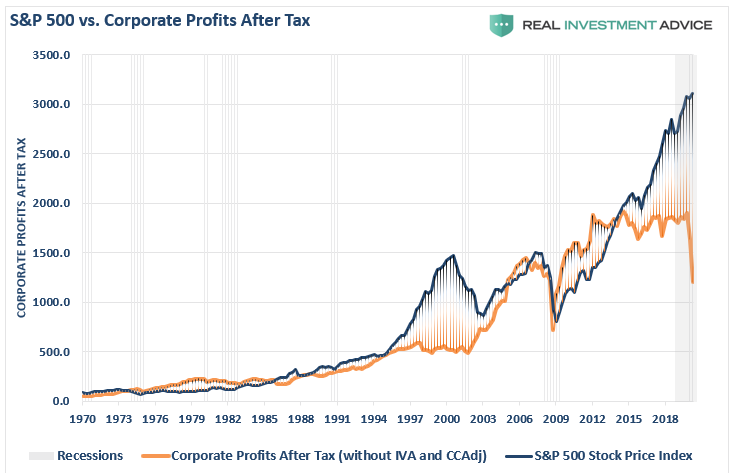

JOHN HUSSMAN COMMENTARY EXCERPT (Hussman Funds)

“Perhaps it’s needless to observe that current valuations

on all of these measures match those of 1929 and 2000. I’ll observe it anyway.

Current valuations are essentially triple those that would be consistent with

historically run-of-the-mill stock market returns of about 10% annually. This

already implies that probable long-term investment returns will be dismal for

passive investors. Notice also that this doesn’t assume any mean reversion at

all. If there is mean-reversion in valuations, as there has been during every

market cycle in history, including those since 2000, the outcome will be

catastrophic for investors over the completion of this cycle, because it

implies a nearly two-thirds loss in the S&P 500 simply to reach pedestrian

historical norms.” – John Hussman, PhD.

CORONAVIRUS (NTSM)

Here’s the latest from the COVID19 Johns Hopkins website

as of 6:30 PM Wednesday. There were about 83,000 new cases reported today. So much for falling numbers. There is a lot

of variability in my numbers since I usually pick them up around 5PM EDT. That’s

only 2 PM on the west coast. With hot-spots

in California reporting later, my daily numbers can be off. When I get the next day’s number, it will

account for any that I missed the day before, so on average, my numbers should

be pretty good. Certainly, the chart of totals is reasonably accurate, except

for yesterday. I had an error in the chart.

“My impression is that while the infectivity of

SARS-CoV-2 is likely due to accessory proteins of the virus that knock down

respiratory defenses, the lethality of COVID-19 (the resulting

disease) is largely due to infiltration and retention of highly inflammatory

blood cells into lung tissue, that then degrade, perforate, and cross through

the alveolar-capillary barrier. The result is cell damage to alveoli (the air

sacs that the lungs use to exchange oxygen with the blood) and to vascular

linings, so that fatality is driven by the combination of oxygen deprivation

and thrombosis. This is not the flu. In recent weeks, we’ve seen rapid outbreaks

in Florida, Texas, and several other states, largely in the same places where

protective measures like distancing and masks were disregarded. This isn’t

really a “second wave.” It’s more like the start-stop profile of local

outbreaks that was predictable even in February. The only surprise is that it

has involved entire states, because somehow, well-understood features of

epidemiology and cell biology have become subjects of wildly ignorant political

debate. Having written on the urgency of containment beginning on February 2,

when the U.S. had only 5 cases and zero deaths, watching this predictable, slow

motion train wreck has been excruciating.” Commentary at…

MARKET REPORT / ANALYSIS

-Wednesday the S&P 500 rose about 0.6% to 3276.

-VIX slipped about 2% to 24.32.

-The yield on the 10-year Treasury slipped to 0.596%.

The S&P 500 Index closed 7.8% above its 200-dMA. 8%

is high and a number in the 10-15% range is a clear pullback signal. Bollinger Bands and RSI are also elevated.

The markets can continue higher, but we’ll keep an eye on these critical

topping indicators.

It’s going to take a big push higher, something like a

blow-off top of several big up-days, to send the Bollinger Bands negative.

The daily sum of 20 Indicators remained +5 (a

positive number is bullish; negatives are bearish). The 10-day smoothed sum

that smooths the daily fluctuations improved from +29 to +33. (These numbers

sometimes change after I post the blog based on data that comes in late.) Most

of these indicators are short-term.

All things considered; I have to be a skeptical Bull

until proven otherwise. There is still room for the Index to run higher;

however, we are getting closer to a pullback of some kind.

MOMENTUM ANALYSIS:

TODAY’S RANKING OF

15 ETFs (Ranked Daily)

The top ranked ETF receives 100%. The rest are then

ranked based on their momentum relative to the leading ETF.

*For additional background on the ETF ranking system see

NTSM Page at…

TODAY’S RANKING OF THE DOW 30 STOCKS (Ranked Daily)

The top ranked stock receives 100%. The rest are then

ranked based on their momentum relative to the leading stock.

For more details, see NTSM Page at…

MICROSOFT (YahooFinance)

“Microsoft (MSFT)

reported quarterly earnings on Wednesday that exceeded Wall Street’s

expectations, as the still-raging coronavirus outbreak proved no match for the

tech giant’s booming cloud computing business. However, the company’s stock —

one of a clutch of high-flying tech stocks that pushed Microsoft’s market cap

well over $1 trillion — fell by nearly 3% in after-hours trading.” Story at…

WEDNESDAY MARKET INTERNALS (NYSE DATA)

Market Internals

remained NEUTRAL on the market.

Market Internals are a decent trend-following analysis of

current market action, but should not be used alone for short term trading.

They are usually right, but they are often late. They are most useful when they diverge from

the Index. In 2014, using these

internals alone would have made a 9% return vs. 13% for the S&P 500 (in on

Positive, out on Negative – no shorting).

Using the Short-term indicator in 2018 in SPY would have

made a 5% gain instead of a 6% loss for buy-and-hold. The methodology was Buy

on a POSITIVE indication and Sell on a NEGATIVE indication and stay out until

the next POSITIVE indication. The back-test included 13-buys and 13-sells, or a

trade every 2-weeks on average.

My current stock allocation is about 40% invested in

stocks. You may wish to have a higher or lower % invested in stocks depending

on your risk tolerance. 40% is a conservative position that I re-evaluate daily.

It is not far below my fully invested position which would be between

50-60%.

As a retiree, 50% in the stock market is about fully

invested for me – it is a cautious and conservative number. If I feel very

confident, I might go to 60%; had we seen a successful retest of the bottom,

80% would not have been out of the question.