Survey says…

Chart and commentary at…

UNPRECEDENTED STOCK MARKET EUPHORIA (Felder Report)

“…note that Rydex traders have been a good contrarian

indicator for a long time. They recently positioned themselves more bullishly

than any time in the history of this fund family, even surpassing the peak seen

during the height of the dotcom mania.”

{kind=link}

“Bull markets are

born on pessimism, grown on skepticism, mature on optimism and die

on euphoria.” -John Templeton

“…With as much money as they are now pouring into the

equity markets, investors might do well to remember that bull markets

aren’t born on euphoria.” – Jesse Felder. Felder Report at….

My cmt: There are 3-charts included in Felder’s

informative blog post and the Bullish Rydex chart was one of them. My work

supports this post even though my Sentiment numbers are based on a different Rydex

ratio: Bulls/(Bulls+Bears). The above

chart is based on a ratio of (Bears+MoneyMkt)/Bulls. Additionally, it uses more

data than mine.

MARKET REPORT / ANALYSIS

-Tuesday the S&P 500 was down about 1.2% to 2344.

-VIX rose about 10% to 12.47.

-The yield on the 10-year Treasury slipped to 2.417%.

(Investors bought bonds.)

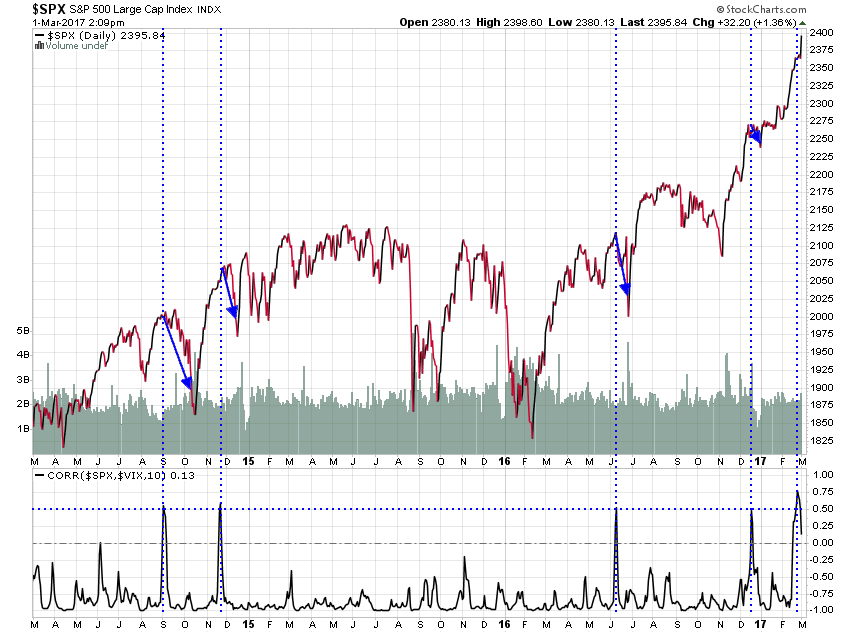

The S&P 500 ended its record-run today. There had been more than 5-months without a

1% down day. So ends the period of extreme calm and, perhaps, an end to

complacency. My sum of 16-indicators declined from +4 to 0. Money trend is flat. There was selling for

most of the day and that followed thru into the afternoon nearly to the close. Breadth

slipped to 48.3% on a 10-day basis, i.e. only 48% of stocks have gone up over

the last 10-days. Only 46% of the volume has been up over the last 10-days. VIX

is still stubbornly low, but not all signs are negative.

Bollinger Bands registered an “Oversold” reading today,

but that is somewhat of an anomaly caused by the Bollinger Band squeeze. The upper

and lower bands were so close together a 1% up-day today would have registered “Overbought”

so it’s hard to place too much faith in the "Oversold" reading. RSI was 27

(14-day, SMA), an Oversold reading, but that too is caused in large part by the

lack of movement in the Index. This time RSI is pointing out that today’s big down-move

is youuuuuge when compared to prior average down-moves; it may not be giving us

a good buy/sell signal. There are more bullish signs.

Most of the ETFs I track were significantly higher Tuesday

in after-hours trading. IWM was up over 2% after-hours, so the dip buyers seem

to be piling in. It will be interesting to check the Rydex long/short funds

tonight when that data is published. The big down-day is likely to be followed

by an up-day Wednesday (true about 62% of the time) based on statistical

analysis. Closing tick (sum of last trades of the day) was a reasonably strong

+172. The most likely finish is still up Wednesday, but there is nothing in

today’s data that suggests the down-trend is over. Volume was about 15% above

the monthly average; that’s a big switch since most volume numbers recently have

been below average, except for the huge volume last Friday associated with

Options Expiration. Volume needs to drop for selling to end.

Bottom line: I don’t think we’ve made a bottom yet, but

it’s possible that a bottom may be near.

The Index is roughly 1% above its 50-dMA and that’s a good support

point. If the 50-day fails it looks like

there is support in the 2270-2290 range. The 200-dMA is 2205 and that’s about 6%

below Tuesday’s close. (That’s another

way of saying I have only guesses about how far down the Index may fall.)

CURRENT RANKING OF 15 ETFs (Ranked Daily)

The top ranked ETF receives 100%. The rest are then

ranked based on their momentum relative to the leading ETF. While momentum isn’t stock performance per

se, momentum is closely related to stock performance. For example, over the 4-months

from Oct thru mid-February 2016, the number 1 ranked Financials (XLF) outperformed

the S&P 500 by nearly 20%.

*For additional background on the ETF ranking system see

NTSM Page at…

I would avoid iEAFE (Europe and Far East); currently its

120-dMA is declining, but its slope is flatter over the past couple of days.

Utilities were up 1.4% on the day, but lost momentum

today due to the nature of moving averages. Utilities (XLU) was the only ETF

among those I track that was positive on the day. The Financials remain number

one, but they are losing momentum while others are gaining. Interest rates are

slipping some and that is bad for the Financials.

Recommended ETF Portfolio of top 3:

1. Financial Select Sector SPDR (XLF)

2. iShares U.S. Aerospace & Defense (ITA)

3. Technology Select Sector SPDR ETF (XLK)

I have not yet established a position based on the ETF

Ranking; I am waiting for a better entry point.

SHORT-TERM TRADING PORTFOLIO - 2017 (Small-% of the

total portfolio)

Rydex 2x Short S&P 500 (RYTPX): Established 6 Dec.

2x Short S&P 500 (SDS): Established 16 Dec.

Long Volatility ETN (VXX): Established 6 Jan 2017.

NET:

Now I wish I had tightened trading rules sooner. I am

underwater again!

-“In a bull market, you can only be long or

neutral.” – D. Gartman

-“The best policy

is to avoid shorting unless a major bear market is underway and downside

momentum has been thoroughly established. Even then, your timing must sometimes

be perfect. In a bull market the trend is truly your friend, and trading

against the grain is usually a fool's errand.” – Clif Droke.

“There are two kinds of forecasters. Those who

don’t know, and those who don’t know they don’t know.”- John Kenneth Galbraith.

TUESDAY MARKET INTERNALS (NYSE DATA)

Market Internals switched

to Neutral on the market.

Market Internals are a decent trend-following analysis of

current market action, but should not be used alone for short term trading.

They are usually right, but they are often late. They are most useful when they diverge from

the Index. In 2014, using these

internals alone would have made a 9% return vs. 13% for the S&P 500 (in on

Positive, out on Negative – no shorting).

LONG TERM INDICATOR

Tuesday, Sentiment was negative (Bullishness is at an

extreme.); Price, Volume & VIX indicators were neutral.

MY INVESTED STOCK POSITION:

TSP (RETIREMENT ACCOUNT – GOV EMPLOYEES) ALLOCATION

I reduced stock allocation to 25% stocks in the

S&P 500 Index fund (C-Fund) Wednesday, 1 March 2017 in my long-term

accounts.

Remainder is 75% G-Fund (Government securities). This is a conservative retiree

allocation based mostly on short-term signals.